The Impact of Vehicle Age on Car Insurance Premiums

Understanding How Vehicle Age Affects Car Insurance Costs

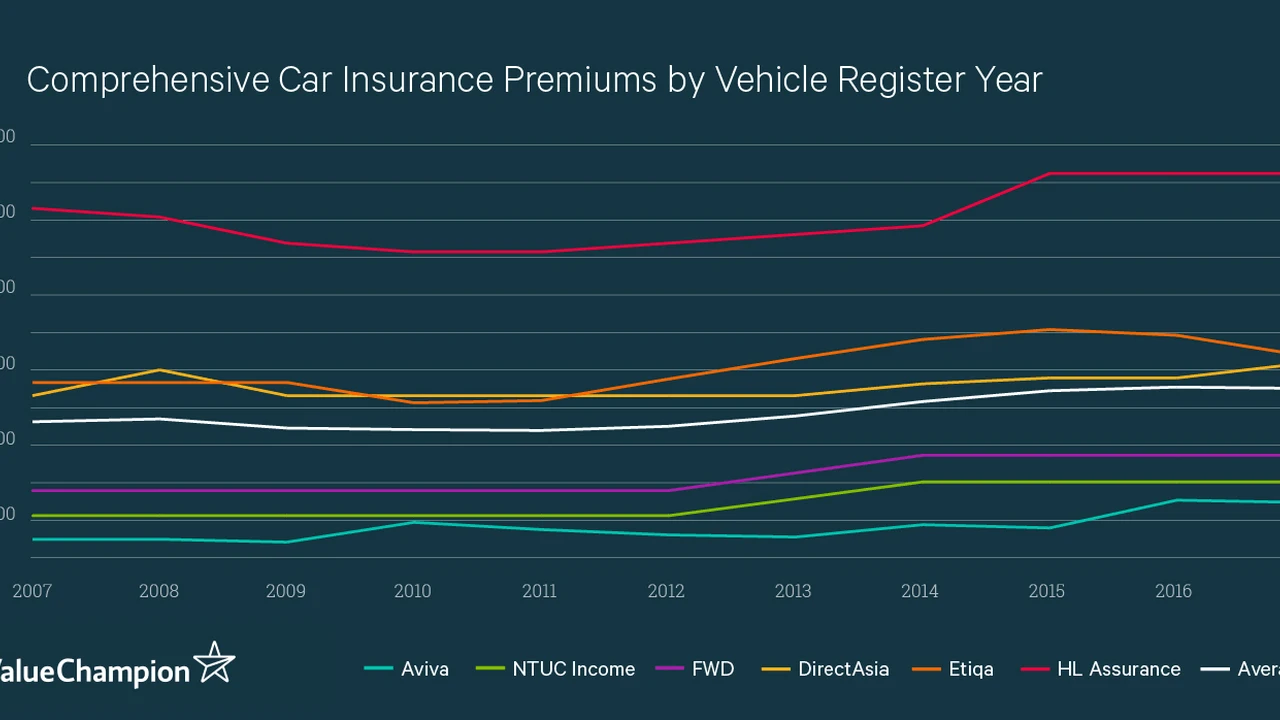

So, you're wondering why your car insurance premium seems to fluctuate more than the stock market? One major factor is the age of your vehicle. It's not just about how *you* drive; insurance companies also consider the statistical likelihood of claims based on the age of your ride. Let's dive into how this works.

Older Cars vs Newer Cars Car Insurance Premiums The Breakdown

Generally speaking, older cars tend to be cheaper to insure than newer ones. Why? It boils down to two primary reasons:

- Lower Replacement Value: If your 1998 Honda Civic gets totaled, the insurance company won't have to shell out as much to replace it compared to a brand-new Tesla.

- Fewer Advanced Safety Features: Older vehicles typically lack the advanced safety tech found in modern cars, such as automatic emergency braking, lane departure warning, and blind-spot monitoring. These features can significantly reduce the risk of accidents, leading to lower premiums for newer cars.

However, there's a twist! Older cars might require more frequent repairs. Parts can be harder to find and more expensive, and the likelihood of mechanical breakdowns increases with age. This can lead to more frequent claims, potentially increasing your premium. It's a balancing act!

Specific Factors Influencing Premiums for Older Vehicles

Several factors contribute to the final car insurance premium for older vehicles:

- Make and Model: Some older cars are inherently more expensive to insure due to their history of claims, repair costs, or theft rates. A classic sports car, even if it's old, will likely cost more to insure than a reliable sedan.

- Driving Record: This is a big one! A clean driving record always helps, regardless of the age of your car. Accidents and traffic violations will significantly increase your premium.

- Coverage Type: The type of coverage you choose also matters. Liability-only insurance is the cheapest option, but it only covers damages to other vehicles or property. Comprehensive and collision coverage offer broader protection but come at a higher cost. For older vehicles, it might not make sense to pay for full coverage if the car's value is relatively low.

- Location: Where you live plays a crucial role. Urban areas with higher rates of theft and accidents tend to have higher premiums than rural areas.

- Mileage: How much you drive also influences your premium. The more you're on the road, the higher the risk of an accident.

Comparing Car Insurance for Different Vehicle Ages

Let's look at a hypothetical scenario. Imagine two drivers, both with clean driving records, living in the same area:

- Driver A: Owns a 2023 Toyota Camry with all the latest safety features.

- Driver B: Owns a 2005 Honda Accord with standard safety features.

Driver A might initially pay a higher premium due to the Camry's higher replacement value. However, the Camry's advanced safety features could earn Driver A discounts, potentially lowering the premium. Driver B's Accord might have a lower initial premium due to its lower replacement value, but the lack of advanced safety features and the increased risk of mechanical issues could offset those savings.

Recommended Safety Features and Their Impact on Car Insurance Rates

Investing in safety features, even for an older vehicle, can sometimes lead to insurance discounts. Here are a few options:

- Anti-Theft Systems: Installing an alarm system or a GPS tracking device can deter theft and potentially lower your premium.

- Backup Cameras: While not always a direct discount, backup cameras can reduce the risk of accidents, which can indirectly help keep your premium low.

- Upgraded Headlights: Brighter headlights can improve visibility and reduce the risk of nighttime accidents.

Exploring Specific Anti-Theft Product Recommendations and Comparisons

Let's delve into some specific anti-theft products you might consider:

- LoJack: A well-known GPS tracking system that helps law enforcement recover stolen vehicles.

- Use Case: Ideal for high-theft areas or for owners who want the peace of mind of knowing their vehicle can be tracked.

- Comparison: More expensive than some other options, but offers a high success rate in vehicle recovery.

- Price: Typically ranges from $700 to $1,000, including installation.

- Viper Alarm System: A comprehensive alarm system with various features, including shock sensors, tilt sensors, and remote starting.

- Use Case: Provides a strong deterrent against theft and vandalism.

- Comparison: Offers more features than basic alarm systems, but can be more complex to install.

- Price: Ranges from $300 to $600, plus installation.

- Ravelco Anti-Theft Device: A unique device that prevents the engine from starting unless a specific plug is inserted.

- Use Case: Highly effective in preventing theft, as it disables the vehicle's electrical system.

- Comparison: More difficult for thieves to bypass compared to traditional alarm systems.

- Price: Around $500 to $800, including installation.

The Role of Comprehensive and Collision Coverage for Older Cars

Deciding whether to carry comprehensive and collision coverage on an older car can be tricky. Here's a breakdown:

- Comprehensive Coverage: Covers damages from events other than collisions, such as theft, vandalism, fire, and natural disasters. If your car is parked outside and susceptible to these risks, comprehensive coverage might be worth considering.

- Collision Coverage: Covers damages to your car resulting from a collision, regardless of who's at fault. If you frequently drive in areas with heavy traffic or high accident rates, collision coverage might be a good idea.

Before purchasing these coverages, consider the actual cash value of your car. If the cost of the coverage exceeds the potential payout in the event of a total loss, it might not be worth it. Get quotes from multiple insurers and compare the premiums and deductibles.

Tips for Lowering Car Insurance Premiums on Older Vehicles

Here are some strategies to help you save money on car insurance for your older vehicle:

- Shop Around: Get quotes from multiple insurance companies. Rates can vary significantly.

- Increase Your Deductible: A higher deductible means you'll pay more out-of-pocket in the event of a claim, but it can lower your premium.

- Bundle Your Insurance: If you have other insurance policies, such as homeowners or renters insurance, bundling them with your car insurance can often result in discounts.

- Maintain a Good Driving Record: Avoid accidents and traffic violations.

- Take a Defensive Driving Course: Some insurance companies offer discounts for completing a defensive driving course.

- Review Your Coverage Annually: As your car ages, reassess your coverage needs and adjust accordingly.

- Ask About Discounts: Don't be afraid to ask your insurance company about available discounts, such as discounts for low mileage, safe driving, or being a member of certain organizations.

Understanding the Impact of Car Modifications on Insurance Costs

Modifying your car, even an older one, can impact your insurance rates. Some modifications, like installing a turbocharger or a lift kit, can increase your premium due to the increased risk of accidents or theft. Other modifications, like adding safety features, might lower your premium.

It's crucial to inform your insurance company about any modifications you make to your vehicle. Failure to do so could result in your claim being denied in the event of an accident.

Exploring Usage-Based Insurance Options for Potential Savings

Consider usage-based insurance (UBI) programs, also known as pay-as-you-drive insurance. These programs track your driving habits using a mobile app or a device plugged into your car. If you're a safe driver who doesn't drive much, you could potentially save money on your premium.

UBI programs typically monitor factors such as:

- Mileage: How much you drive.

- Driving Time: When you drive (e.g., daytime vs. nighttime).

- Hard Braking: How often you brake abruptly.

- Acceleration: How quickly you accelerate.

- Speed: How often you exceed the speed limit.

The Future of Car Insurance and Vehicle Age

As technology advances, the way insurance companies assess risk is constantly evolving. The increasing prevalence of autonomous driving features and connected car data will likely play a significant role in determining premiums in the future. It's possible that vehicle age will become less of a factor as insurance companies rely more on real-time driving data to assess risk.

:max_bytes(150000):strip_icc()/277019-baked-pork-chops-with-cream-of-mushroom-soup-DDMFS-beauty-4x3-BG-7505-5762b731cf30447d9cbbbbbf387beafa.jpg)